NGFS provides a path for the banking industry to fight back

The Network for Greening of the Financial System (NGFS) recently published the second phase of its framework for the economic impact of climate change and mitigation policies. In this article we review the framework and its importance in fighting climate change.

NGFS started in 2017 as a working group of central banks and regulators with the mission to translate the scientific pathways (being created by groups such as the IPCC) and policy commitments and announcements made by governments into economic scenarios and outcomes. There are currently 95 members of the NGFS, including the US, EU, Brazil, Japan, UK, and China.

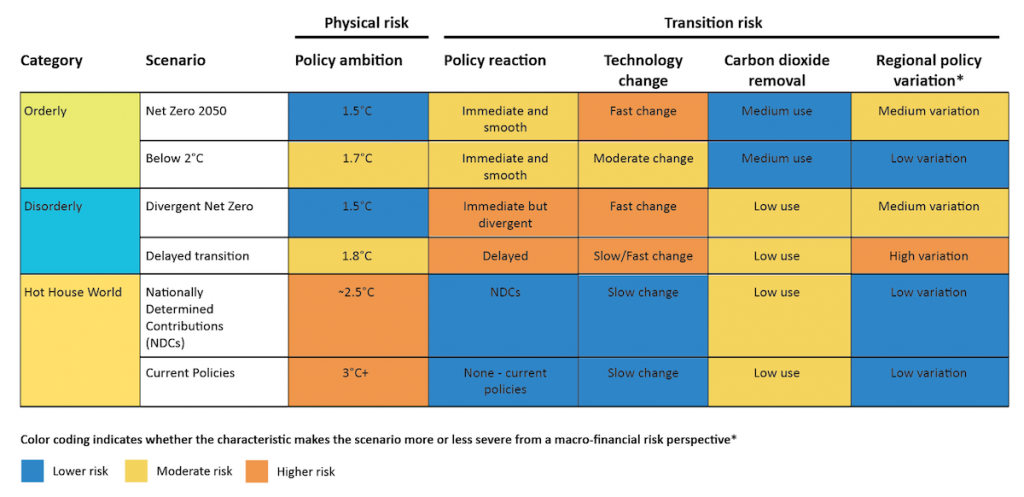

NGFS scenarios are defined by the resultant global temperature rise by 2100 and designated by the manner they are achieved. The scenarios are also split between physical (actual impact from climate change) and transition (impact from mitigation strategies and policies) risks.

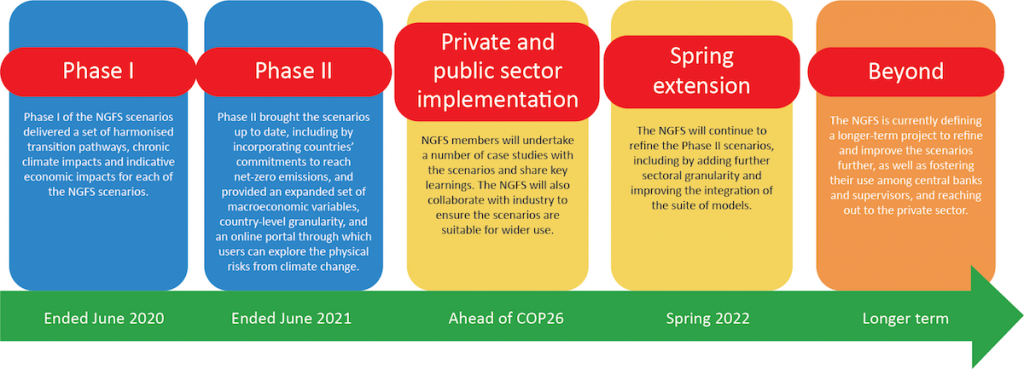

This is an effective working framework that is continually refined and is working towards COP26 (The next big climate change conference to be held in Glasgow in November 2021) and beyond.

NGFS’ mission is to create a viable top-down approach that can first be used as a common framework for central banks and planners, but can also be progressively adopted by the private sector.

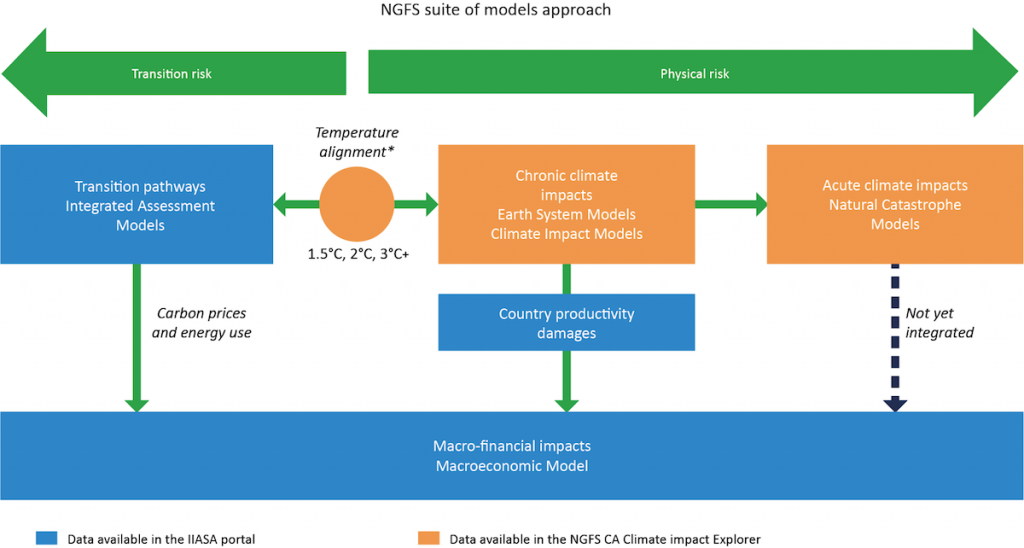

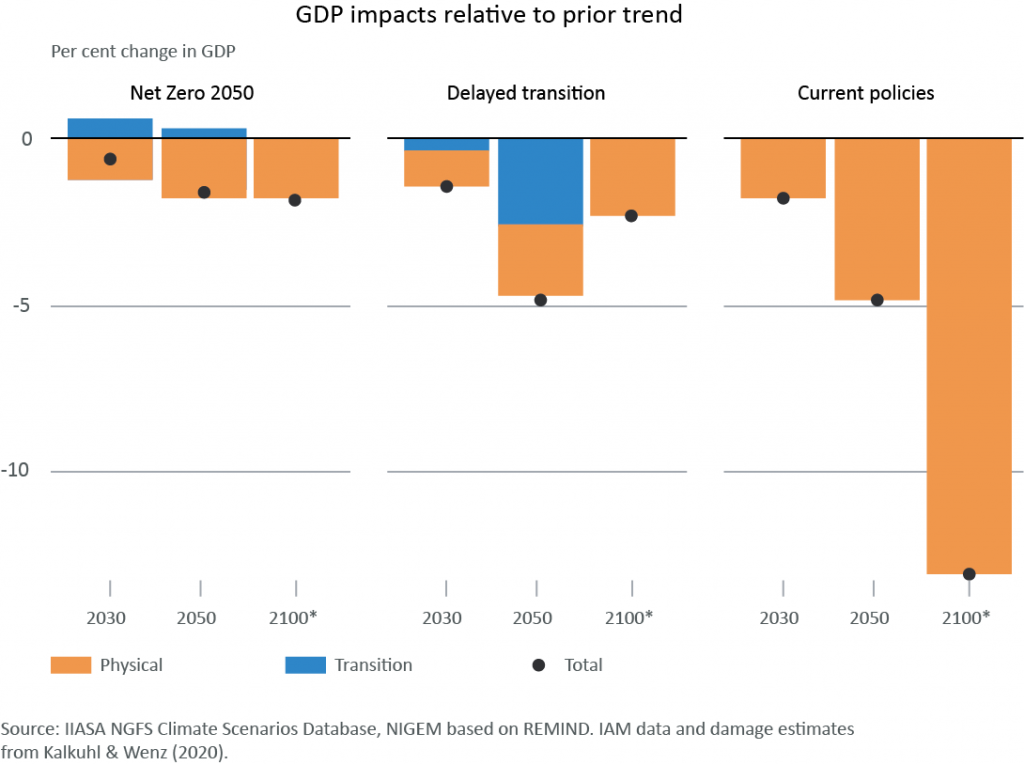

The applicability and effectiveness of the scenarios become apparent in the second stage of the adoption by the private sector. A high-level overview of the framework illustrates how the top-down impacts on GDP are estimated.

These are then transformed into overall GDP impact based on policy status and implementation speed across various countries.

Importantly, the NGFS examines the economic indicators in each country, including, inflation, interest rates, unemployment, and across the sectoral span of those economies.

NGFS is an evolving undertaking – the second phase has more refined scenarios as well as their usage and explanations.

For banks, these scenarios are an ideal starting point for their individual climate-based analysis. They are created by the regulatory bodies that have jurisdiction over banks. The scenarios encompass much of the work involved in translating established science into tangible economics.

To utilize these scenarios, banks have to translate their balance sheets into correlated impacts as starting points to assess potential impacts to credit profiles of their underlying obligors. This impact is likely to create liquidity impact as scenarios become real. Deterioration in obligor creditworthiness would require higher capital provision, in turn impacting their overall capital base. The aggregate impact on systemic capital would impact the a sustainable future for the climate.

Banks are advised to study and apply these scenarios and take an active role in the fight against climate change.