In 2020, the European Central Bank (ECB) released its guidance for inclusion of climate change in risk management frameworks. The 2022 survey conducted by the Central Bank shone a light on where the industry is in its journey and how much further it has to go.

The ECB issued guidance on how financial institutions should incorporate climate-related risks into existing frameworks…

The ECB’s ‘Guide on climate-related and environmental risks’ was written with the aim of clearly laying out how directly supervised institutions must incorporate both physical and transition-related risks into their existing risk frameworks. It was also clear that it was intended to be a risk management blueprint for all banks across the EU bloc.

Covering ‘Risk Appetite’, ‘Risk Frameworks’, ‘Credit Risk’, ‘Liquidity Risk’, ‘Market Risk’, ‘Operational Risk’, and ‘Risk Reporting’, the guide explicitly speaks to climate-specific stress testing and scenario analysis. The supervisory expectations were as follows at a high level:

Overview of ECB supervisory expectations

- Institutions are expected to understand the impact of climate-related and environmental risks on the business environment in which they operate, in the short, medium and long term, in order to be able to make informed strategic and business decisions.

- when determining and implementing their business strategy, institutions are expected to integrate climate-related and environmental risks that impact their business environment in the short, medium or long term.

- The management body is expected to consider climate-related and environmental risks when developing the institution’s overall business strategy, business objectives and risk management framework, and to exercise effective oversight of climate-related and environmental risks.

- Institutions are expected to explicitly include climate-related and environmental risks in their risk appetite framework.

- Institutions are expected to assign responsibility for the management of climate-related and environmental risks within the organisational structure in accordance with the three lines of defence model.

- For the purposes of internal reporting, institutions are expected to report aggregated risk data that reflect their exposures to climate-related and environmental risks with a view to enabling the management body and relevant sub-committees to make informed decisions.

- Institutions are expected to incorporate climate-related and environmental risks as drivers of existing risk categories into their existing risk management framework, with a view to managing, monitoring and mitigating these over a sufficiently long-term horizon, and to review their arrangements on a regular basis. Institutions are expected to identify and quantify these risks within their overall process of ensuring capital adequacy.

- In their credit risk management, institutions are expected to consider climate-related and environmental risks at all relevant stages of the credit-granting process and to monitor the risks in their portfolios.

- Institutions are expected to consider how climate-related and environmental events could have an adverse impact on business continuity and the extent to which the nature of their activities could increase reputational and/or liability risks.

- Institutions are expected to monitor, on an ongoing basis, the effect of climate-related and environmental factors on their current market risk positions and future investments, and to develop stress tests that incorporate climate-related and environmental risks.

- Institutions with material climate-related and environmental risks are expected to evaluate the appropriateness of their stress testing with a view to incorporating them into their baseline and adverse scenarios.

- Institutions are expected to assess whether material climate-related and environmental risks could cause net cash outflows or depletion of liquidity buffers and, if so, incorporate these factors into their liquidity risk management and liquidity buffer calibration.

- For the purposes of their regulatory disclosures, institutions are expected, to publish meaningful information and key metrics on climate-related and environmental risks that they deem to be material, with due regard to the European Commission’s Guidelines on non-financial reporting: Supplement on reporting climate-related information.

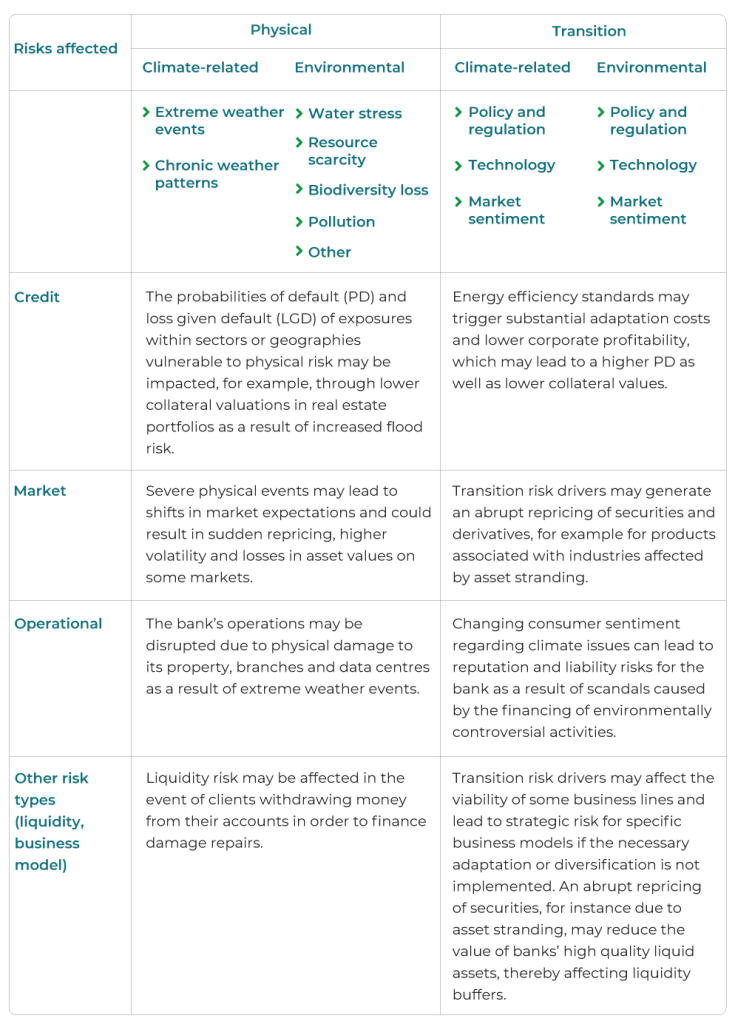

The guidance makes it clear that financial institutions must treat both transitional and physical climate risk as drivers of existing risk categories, specifically pointing to how the costs of transitional policies will likely cause increased credit spreads and potentially impact national GDPs during that transition.

It is also mentioned that the costs of this transition and the costs of dealing with the physical impacts are highly correlated and largely dependent upon the speed and nature of the transition. There are choices to be made between orderly and disorderly transition routes, as well as climate targets, expressed as ultimate global warming limits by the end of this century.

The climate guidance invokes the Capital Requirements Directive (CRD)…

The CRD, specifically articles 73 and 74, require institutions to implement internal governance and processes that ensure effective and prudent management. This must include the identification, assessment and monitoring of climate change on the business environment that they operate within. This must include geographic and sector-specific degradation brought about by climate change and policies designed to mitigate it.

The ECB also point out that these recommendations are explicitly covered by requirements specified in the ‘Internal Capital Adequacy Assessment Process’ (ICAAP)

Risk management frameworks are expected to carry much of the weight for compliance…

The guidance document lays down several expectations of risk management, including:

- Incorporation of climate-related risks as drivers of existing risk categories, with a view to managing, monitoring, and mitigating over short-, mid- and long-term time horizons.

- Consideration of climate-related risks at all stages of the credit granting and risk monitoring process.

- Consideration of how climate-related events may impact their own business continuity and any impacts that may have on their liability or reputation.

- Developing stress tests that monitor potential impacts on their market risk positions and future investments.

- Examining existing stress testing capabilities with a view to evaluating them for climate-related appropriateness.

- Assessment of climate-related risks to net cash outflows and/or liquidity buffers.

The highest focus is given to the credit risk section, as would be expected due to its capacity to deteriorate the profitability, liquidity and, ultimately, viability of a financial institution through capital requirement escalation.

Climate-related credit risks are expected to be part of loan origination and pricing and are constantly monitored. Climate-related in this context, includes:

- Exposure to physical hazard

- Potential increases in default risk

- Client risk mitigation measures

- Development of climate-related risk limits

- Climate-related deleveraging strategies

One suggestion from the ECB is the development of ‘Climate-informed shadow probabilities of default’, which could be reported in parallel.

As expected, liquidity risk is also a concern, and the ECB may also invoke the ‘Internal Liquidity Adequacy Assessment Process’ (ILAAP), encouraging institutions to include direct and indirect impacts of climate-related risks in their reporting. They specifically focus on the potential erosion of the value of liquidity buffers through the falling value of ‘High Quality Liquid Assets’ (HQLA).

Regarding appropriate stress tests, institutions are encouraged to use a variety of scenarios in line with pathways developed by the ‘Intergovernmental Panel on Climate Change’ (IPCC). Scenarios used for stress testing must include:

- How the institution may be affected by physical risk and transition risk.

- How climate-related risks may evolve under various scenarios, taking into account that these risks may not be reflected in historic datasets.

- How climate-related risks may materialize over short, mid and long terms.

The guidance also covers internal roles and responsibilities and disclosures.

These should be included in the overall planning by financial institutions.

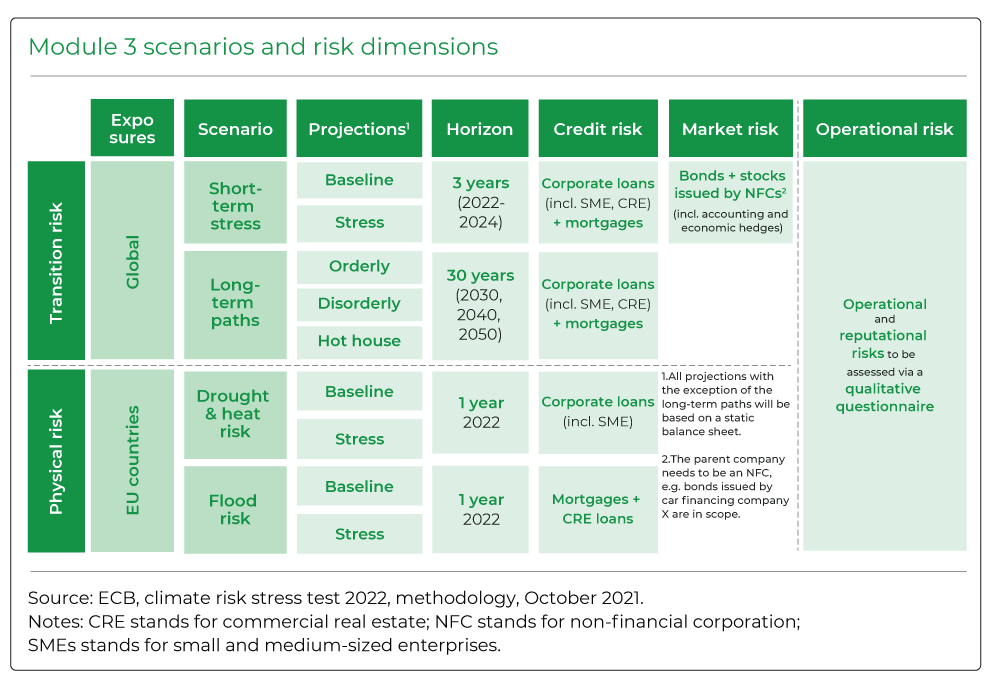

2022 saw a European wide assessment of bank readiness for climate risk inclusion…

The ECB surveyed 104 significant institutions with the aim of determining how far banks had integrated climate-related risks into their risk management. Specific aims included:

- Progress banks have already made in developing climate risk stress-testing frameworks;

- Capacity of banks to produce climate risk factors, an intermediate step towards developing climate risk stress test estimates;

- Capacity of banks to produce climate risk stress test projections;

- Risks banks are facing in the form of transition risks (both short-term and long-term) and acute physical risk events.

The central bank looked at qualitative assessments, risk factor stock takes and also ran qualitative stress tests based upon scenarios and metrics from the ‘Network for Greening the Financial System’ (NGFS), covering both transition and physical risks. The scenarios used for the qualitative part of this exercise covered short- and long-term horizons. as well as multiple climate pathways. There was a focus on residential mortgages and corporate loans.

Ultimately, the ECB gained an insight into both potential losses to the European financial system arising from physical climate change and transitional policies, as well as the readiness of surveyed banks to manage those risks in a prudent manner.

Findings included:

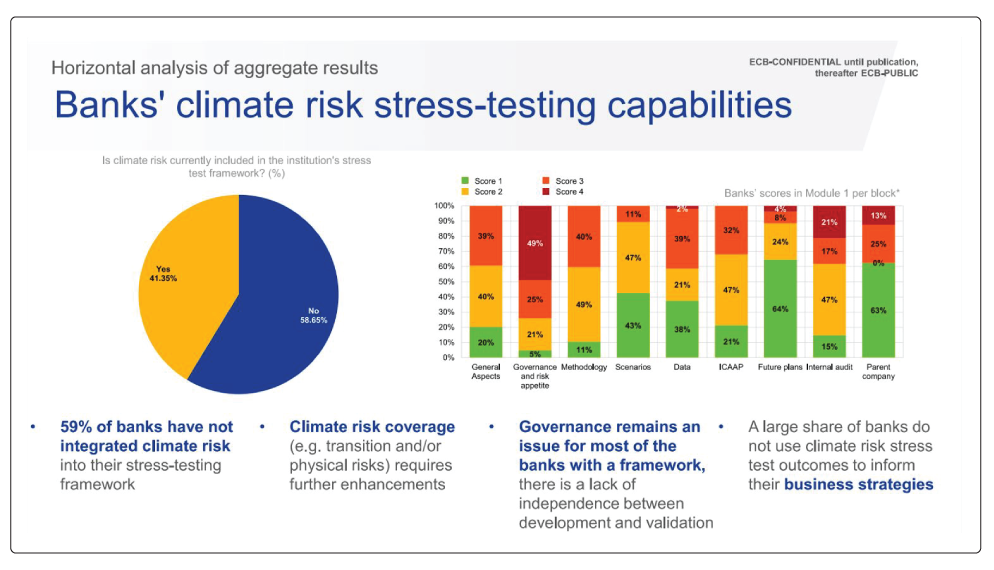

- Slow integration of climate risk into risk management and stress testing.

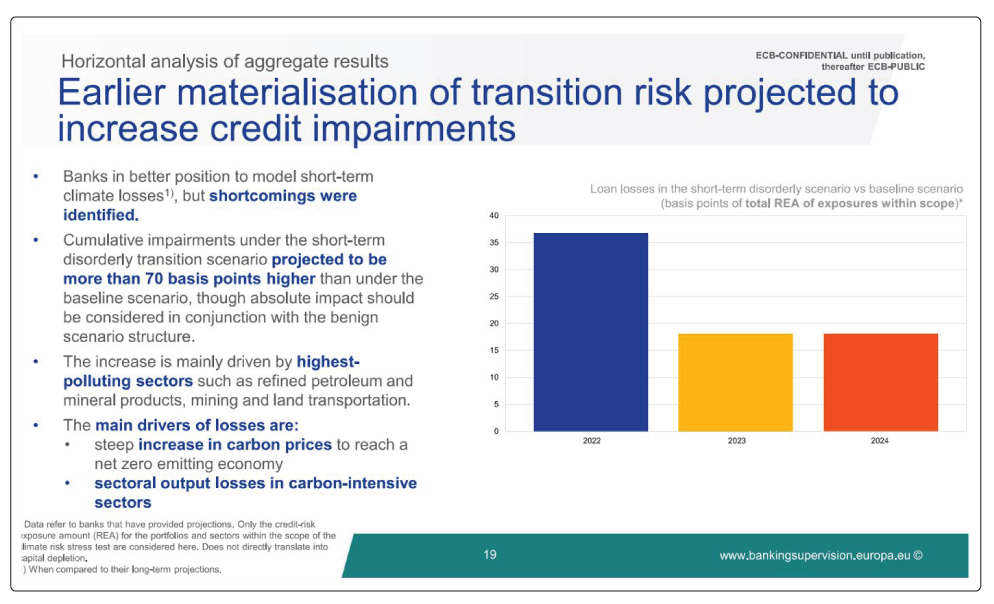

- Early materialization of transition risk may significantly increase credit impairments

Ultimately, the ECB concluded with six strong recommendations:

- Banks need to integrate climate risk stress into their ICAAPs.

- Banks need to enhance their climate risk stress-testing frameworks to account for various transmission channels and asset classes, covering physical and transition risks.

- Banks need to establish a robust governance structure for their climate risk stress-testing frameworks and integrate climate risk stress tests into their banking activities.

- Banks need to incorporate climate risk scenarios into their stress-testing models, both transition and physical.

- Banks should enhance climate risk management, understand their client’s transition plans and strengthen their strategic plans to exploit the opportunities of a green transition.

- Banks need to invest much more in climate-relevant data collection by engaging with customers and improving their proxy assumptions.

Banks need to take action…

All banks must consider the speed at which the ECB rolled out its guidance and how it is testing its directly-governed institutions. It is highly likely that these recommendations will become general reporting requirements sooner rather than later.

Of course, it must also be borne in mind that the reason for this speed of action is because the ECB recognizes the material risk that climate change represents to the European financial system.

Financial institutions need to extend their risk management systems in ways that can capture specificities of climate-related threats. At a minimum, they must:

- Develop the means to understand how multiple physical climate pathways may impact their customers and their credit profiles.

- Understand how transition policies built into these pathways may deteriorate the business models of their corporate customers.

- Work with customers to create adaptation plans to protect them from the worst effects and avoid business losses and stranded assets.

- Include potential climate-specific losses as a range and as a standard in their capital and liquidity reporting.

Because of the unique nature by which IPCC climate pathways are created, it will be necessary to use deterministic scenarios for climate-specific stress tests and analysis rather than reusing historically calibrated stochastic processes already in place.

Climate-specific scenarios have been covered in –

And

Global regulation advances have been covered in –

GreenCap can help…

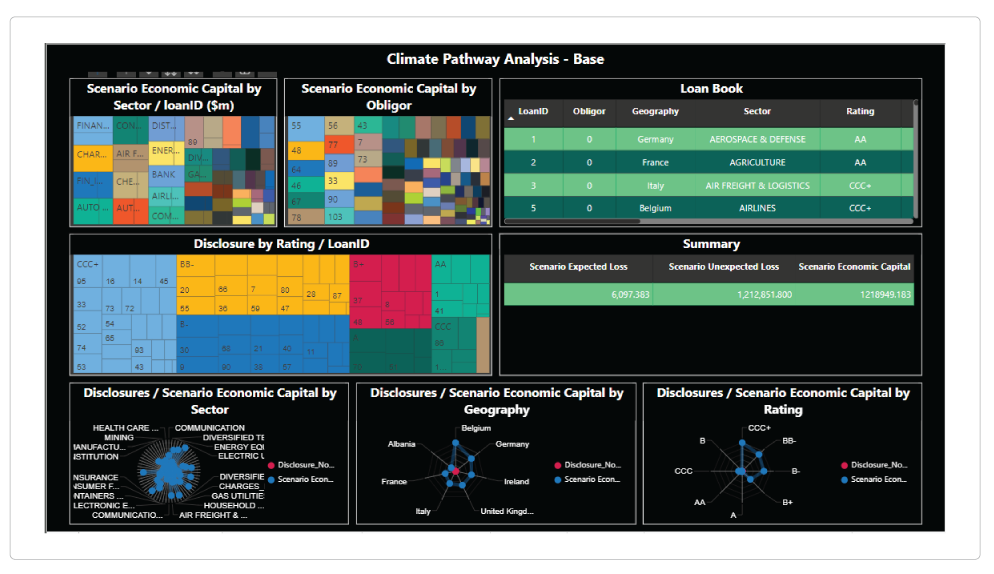

GreenCap is a ‘Risk As A Service’ (RaaS) solution that enables banks to run transitional and physical risk assessment against their balance sheet that reports individual loan and portfolio level, providing:

- Implied PD changes across multiple climate pathways

- Economic capital changes – Broken into expected and unexpected losses

- Implied spreads on climate-impacted loans

The system supports multiple scenarios and pathways and allows bottom-up adaptations to be added at the customer level for fine-tuning risks and exposures. As a cloud service, GreenCap is extremely fast to implement and use for exactly the type of analysis that is being asked for by the ECB and other Central Banks around the world.

Scenario

Scenario

GreenCap is designed to be used by banks of all sizes.

Visit GreenCap.live for more insights and resources designed to assist banks in navigating the challenges posed by climate change and policies introduced to mitigate it.