Recent problems at Credit Suisse, Silicon Valley Bank and Signature Bank have rekindled market fears around liquidity and stability within the banking sector. It is worth using this moment to consider how destabilizing climate change may be to the sector.

Banking liquidity is defined in highly specific ways…

Specific liquidity ratios exist that serve as singular measures of the strength of a bank. These include:

Liquidity Coverage Ratio (LCR) – Proportion of High-Quality Liquid Assets (HQLA) that a bank needs to hold in order to continue to meet their short- and mid-term obligations.

Net Stable Funding Ratio (NSFR) – A liquidity standard that requires banks to hold enough stable funding to cover their long-term assets (assets with durations of greater than one year).

These ratios are, though, just snapshots. In 2008, the Basel Committee on Banking Supervision (BCBS) released its ‘Principles of sound liquidity risk management and supervision’, which detailed the best practices for banks to ensure their liquidity, and by extension, market stability.

The section within this document that covers risk management includes the following principles:

Principle 5: A bank should have a sound process for identifying, measuring, monitoring, and controlling liquidity risk.

Principle 6: A bank should actively monitor and control liquidity risk exposures and funding needs within and across legal entities, business lines, and currencies.

Principle 7: A bank should establish a funding strategy that provides effective diversification in the sources and tenor of funding. It should maintain an ongoing presence in its chosen funding markets and strong relationships with funds providers.

Principle 8: A bank should actively manage its intraday liquidity positions and risks to meet payment and settlement obligations on a timely basis under both normal and stressed conditions.

Principle 9: A bank should actively manage its collateral positions, differentiating between encumbered and unencumbered assets.

Principle 10: A bank should conduct stress tests on a regular basis for a variety of short-term and protracted institution-specific and market-wide stress scenarios to identify sources of potential liquidity strain and to ensure that current exposures remain in accordance with a bank’s established liquidity risk tolerance.

Principle 11: A bank should have a formal contingency funding plan (CFP) that clearly sets out the strategies for addressing liquidity shortfalls in emergency situations.

Principle 12: A bank should maintain a cushion of unencumbered, high-quality liquid assets to be held as insurance against a range of liquidity stress scenarios, including those that involve the loss or impairment of unsecured and typically available secured funding sources.

Taken together, these ‘best practices’ demand that banks assess their liquidity against multiple stress tests, with a view to ensuring that there is a buffer of cash or cash equivalents (typically government paper with a short-dated maturity).

The principles need to be considered and incorporated into bank governance, including those covering new business initiatives or emergent risks. Climate change falls into both of these categories.

Climate change is introducing risks that will impact banks’ capacity to manage their liquidity risk…

The same BSBC has been looking at the particularities of climate change, and has augmented the risk management advice with a paper released in June 2022 – Principles for the effective management of climate-related financial risks.

The 12 key principles intended for banks are as follows:

Principle 1: Banks should develop and implement a sound process for understanding and assessing the potential impacts of climate-related risk drivers on their businesses and on the environments in which they operate.

Principle 2: The board and senior management should clearly assign climate-related responsibilities to members and/or committees and exercise effective oversight of climate-related financial risks.

Principle 3: Banks should adopt appropriate policies, procedures, and controls that are implemented across the entire organization to ensure effective management of climate-related financial risks.

Principle 4: Banks should incorporate climate-related financial risks into their internal control frameworks across the three lines of defense to ensure sound, comprehensive and effective identification, measurement and mitigation of material climate-related financial risks.

Principle 5: Banks should identify and quantify climate-related financial risks and incorporate the ones assessed as material over relevant time horizons into their internal capital and liquidity adequacy assessment processes, including their stress testing programs where appropriate.

Principle 6: Banks should identify, monitor and manage all climate-related financial risks that could materially impair their financial condition, including their capital resources and liquidity positions. Banks should ensure that their risk appetite and risk management frameworks consider all material climate-related financial risks to which they are exposed and establish a reliable approach to identifying, measuring, monitoring, and managing those risks.

Principle 7: Risk data aggregation capabilities and internal risk reporting practices should account for climate-related financial risks.

Principle 8: Banks should understand the impact of climate-related risk drivers on their credit risk profiles and ensure that credit risk management systems and processes consider material climate-related financial risks.

Principle 9: Banks should understand the impact of climate-related risk drivers on their market risk positions and ensure that market risk management systems and processes consider material climate-related financial risks.

Principle 10: Banks should understand the impact of climate-related risk drivers on their liquidity risk profiles and ensure that liquidity risk management systems and processes consider material climate-related financial risks.

Principle 11: Banks should understand the impact of climate-related risk drivers on their operational risk and ensure that risk management systems and processes consider material climate-related risks.

Principle 12: Where appropriate, banks should make use of scenario analysis to assess the resilience of their business models and strategies to a range of plausible climate-related pathways and determine the impact of climate-related risk drivers on their overall risk profile.

The unmissable message here is that climate-specific risk management needs to be added to existing risk frameworks. Specifically, plausible scenarios should be used to identify risk drivers and resultant impacts on the banks’ business and liquidity.

The 2008 and 2022 principles need to be seen as complementary…

Stress testing the impacts of climate change on banks’ liquidity must take into account the fact that, from an economic model perspective, what is being proposed is a wholesale paradigm shift. Scenarios need to be built on the following pillars:

- Transitional climate-related policies will create regulations/taxes/fines that impact borrowers whose loans make up the balance sheets of the bank.

- Increased pressure on revenue through investment in simply complying with new regulations, will impact borrowers’ risk profiles and the resultant economic capital that will need to be held by the bank against these loans.

- There are multiple climate pathways with differing transitional and physical climate outcomes that have been developed by the ‘Intergovernmental Panel on Climate Change’ (IPCC), as well as individual ‘Nationally Determined Contributions’ (NDCs) from 196 countries.

In order to properly understand the potential liquidity requirements created under these scenarios, banks must develop economic stress tests that can apply the costs, estimated by the ‘Network for Greening the Financial System’ (NGFS) economists and central bankers, to the policies that are already in place, committed to, through the NDC and implied by the wider UN commitment to hold global warming to 2 degrees above pre-industrial levels by 2100.

Effective stress tests also need to allow climate adaptations already made by borrowers to be reflected by reducing the future financial impact on the borrower and bank’s economic capital. This effectively means starting with a top-down approach, but adding nuance from bottom up, loan level adjustments.

The results of the stress tests must include, per stress, expected deterioration in credit scores as well as increases in economic capital for each loan. The cumulative effect will inform the liquidity group within the risk committee to properly develop a contingency liquidity plan that matches the outcomes by climate pathway.

Building climate scenarios has been covered in – Constructing a feasible approach to climate-related credit risk and Creating Meaningful Climate Change Scenarios in a Changing World

Governance is vital to risk management…

Once the underlying numbers have been computed, banks must then build into their risk frameworks:

- Regular reporting of potential liquidity outcomes as local and global climate policy direction becomes clearer.

- Target outcomes in economic capital terms that align with any public statements made by the bank.

- Increasingly detailed adaptations as various economic sectors develop their own guidelines and rules.

- Limits on loans and loan pricing that take the expected climate effects into account and can be applied as the first line of defense.

Incorporating climate risk into existing risk frameworks is covered in – Expectations of climate risk management are growing and banks must create their frameworks now

Aligning sustainability goals with risk management is covered in – 6 principles banks need to adopt to thrive in the upcoming green economy

There is no doubt that properly reflecting climate-related financial impacts in banks’ risk management frameworks and appetites will take significant work and involve multiple bank divisions. The result, however, will enable those banks that invest in the effort to avoid the liquidity shocks that are likely to be one of the most turbulent aspects of the transition to a greener global economy.

GreenCap can help…

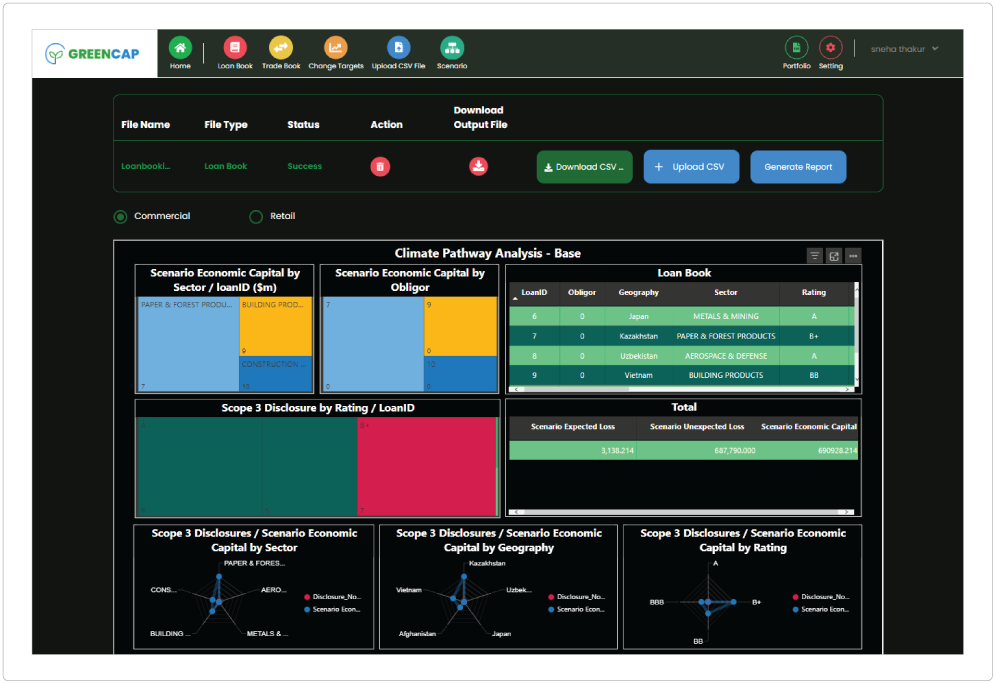

GreenCap is a ‘Risk as a Service’ (RaaS) solution that gives banks the capacity to build meaningful climate scenarios that mirror the multiple available climate pathways and stress test their balance sheets.

The results produced by the system include:

- Changes, by scenario, in borrower risk ratings

- Implied spreads, by loan, needed to make up borrower credit deterioration under each scenario

- Increase in economic capital, broken into expected and unexpected losses

- Targets and limits to be applied and monitored by risk management and lending officers

GC main screen (corporate)

GC main screen (retail)

GreenCap is designed to fill the gap in risk frameworks that need deterministic climate stress tests in a way that can be transparently used by the risk governance committee to meet the best practices recommended by the BCBS.