COP27, which concluded in Egypt recently, was held at a time of rampant international energy price inflation, a land war in Europe, and against a history of increasing intransigence in specific areas of funding. Even so, some achievements of the conference are well worth noting by banks.

History dealt COP27 a difficult hand to play…

Developing countries have called for two specific things for a long time.

The first is ‘Loss and Damage’ payments from developed nations. Essentially, some countries find themselves at the forefront of physical climate change impacts, which are primarily caused by developed countries. The situation is exacerbated by the fact that even now, richer countries emit many multiples of the greenhouse gasses coming from the worst-affected nations in the world. Historically, wealthier countries have fought against this, as it could conceivably lead to legal claims in the future.

The second, linked, issue is that smaller coastal and island nations desperately need the wider global community to reinforce a commitment to holding global warming this century to 1.5 degrees above pre-industrial levels. If higher targets are allowed to become a replacement for 1.5 as the target, then the damages they would sustain could threaten any viability they have as independent countries, if not wipe them out entirely.

With the COP coming as the Russian invasion of Ukraine has seen energy prices skyrocket, which itself has led inflation upwards, western spending conversations have been more towards military and energy security than climate change.

Since Glasgow, the scientific warnings have only become louder…

At the 26th edition of the COP in 2021, scientific evaluations of the combined Nationally Determined Contributions (NDCs), put forward by countries as a requirement from the Paris accord, reached in 2015, alarmingly predicted that even full rollouts of the plans would see a century end increase of 2.7 degrees. This would be a disaster for the smaller developing nations. Delegates agreed to revisit and strengthen their NDCs in time for the 2022 COP.

As the conference started, very few had done so, and revised analysis showed that the reduction in emissions by 2030 would be around 1% only, a long way from the 43% total reduction needed for 1.5 degrees to be even remotely possible.

There were some green shoots of hope…

Surprisingly, there was more progress on the ‘Loss and Damage’ issue than had been seen at any prior COP. The group agreed that a fund ought to be set up, and a transitional committee was created to determine how such a fund would be filled and subsequently run. The key part of this section of the agreement is that outside of some ‘pledges’, the funding was not determined, and will likely be a mix of public and private initiatives. These, along with the organizational recommendations, are due to be presented to COP28 in the UAE next year.

There was also increased pressure on banks and development banks to ease the flow of money for transitional projects, with a new vision being asked for, in order that such institutions are ‘fit for purpose’ over the next decade.

As well as continued black holes…

Curtailing carbon emissions depends to a large degree on reaching peak use for fossil fuels sooner rather than later. One proposal mooted was for the summit to agree to a commitment to phase out all fossil fuels, which would have significantly strengthened the Glasgow position. This was not adopted, and it was noted by the Glasgow COP President, Alok Sharma, that to reach the ambitious goal of 1.5, carbon emissions need to peak by 2025, and that this not being committed to represented a significant failure of the conference.

All in all, a disappointing but mixed bag of results…

The easy conclusion is that this COP failed to achieve progress substantively, and that this was a sadly predictable outcome, given the geopolitical situation framing it. This misses some important nuances though that banks, in particular, would do well to take note of.

The fact is that a fund has been agreed to, whereby emitters will effectively pay in, while those suffering climate hardship will take out. Even without details, this should put banks on alert that money will need to be raised from the private sector, with the higher emitting industries most likely to be targeted for whatever proposals ultimately come forward. Conceivably, funds could be raised from:

- Wider adoption of Carbon ‘cap and trade’ schemes, which have the advantage of locking in a base level of energy security as well as charging for emissions or the introduction of carbon tax schemes.

- Creation of carbon border adjustments to prevent such schemes from simply incentivizing offshoring of CO2 emissions.

Any or all of the above would act as a profit drag to ‘brown’ industries and firms, as well as an additional bonus for those companies already investing in ‘greening’ their operations. The implications for future costs and credit profiles are significant, as it threatens to turn the economic order on its head, with fossil fuel utilities becoming a greater risk to bank balance sheets than sustainable start-ups.

Another potential impact of a ‘Loss and Damage’ fund is that governments may escape historic ‘reparation’ payments, but subsidizing future emission growth could carry high financial penalties once the president for the fund is in place.

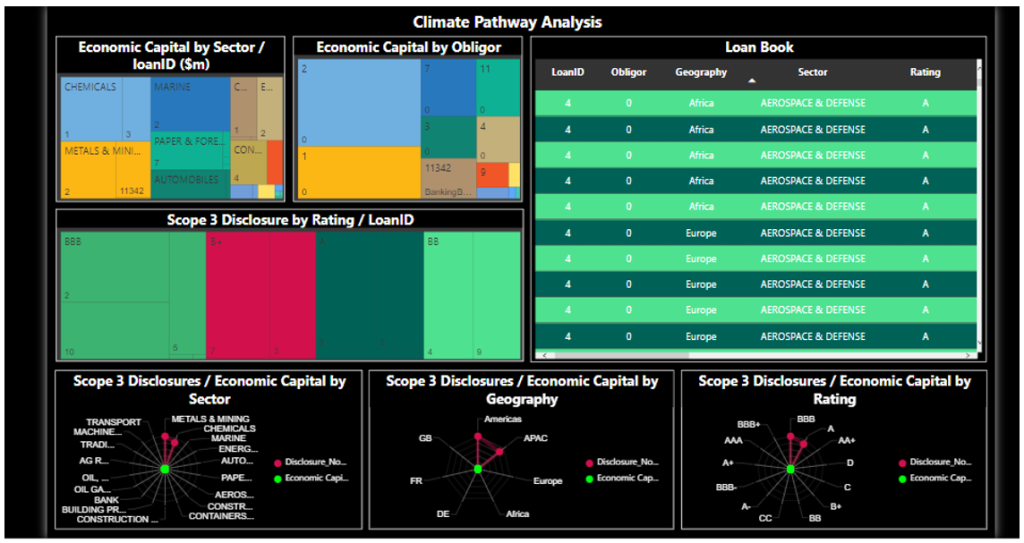

These should be considered by banks, as they choose lending strategies going forward, or else they may find that their credit risk costs outweigh any short-term gains to be had from a ‘business as usual’ approach. Climate scenario analysis, centering on transitional costs and how they may be borne, needs to become a staple reporting requirement in every bank’s risk department.

GreenCap can help…

GreenCap is a turnkey, ‘Risk as a Service’ (RaaS) solution that gives banks the capacity to run multiple climate scenarios and pathways and view the impact they have on:

- Loan pricing

- Balance sheet profitability

- Expected and unexpected losses (credit risk capital)

- Borrowers’ probability of default

GreenCap is built on the philosophy that banks need a solution that allows them to view climate change in banking terms. Without such a solution, they are caught between current banking rules around credit risk and the urgent need to finance the transition to a sustainable economic future.