Calibrating climate scenarios will require banks’ risk departments to navigate the vagaries of global carbon budget management. This requires an understanding of what it involves and what it really entails.

The carbon budget is a consequence of the 2100 global warming target…

In 2015, at the Conference Of Parties (COP) in Paris, the world’s governments committed to holding global warming to 2 degrees above 1990 levels, while making best efforts to achieve a 1.5-degree limit.

This target is calibrated by using the heating potency of CO2 and calculating the cumulative amount of the gas in the atmosphere that would create it. The current atmospheric CO2 level can be measured with reasonable accuracy. It is also known that every gigaton (Gt) of carbon burned creates 3.67Gt of CO2.

For a 2100 limit of 2 degrees, the remaining carbon budget is 1150Gts of CO2, but for 1.5 degrees it is just 400Gts.The current global rate of CO2 emission is 42Gts p/a and still trending up.

The life of the remaining budget, however, is subject to a number of variables…

The total amount of CO2 that can be allowed to be released each year, is a function of the cumulative target, and how much CO2 will be sequestered.

Oceans and Forests act as vital carbon sinks, actively absorbing CO2. Between 2010 and 2019, 21.7Gt of CO2 was removed from the atmosphere by these ecosystems. In 2020, over half (54%) of the gas emitted was absorbed, but this is viewed as anomalous, due to the overall 7% fall in emissions, as a result of the global COVID pandemic. Also, it is far from clear whether this rate of sequestration can be sustained.

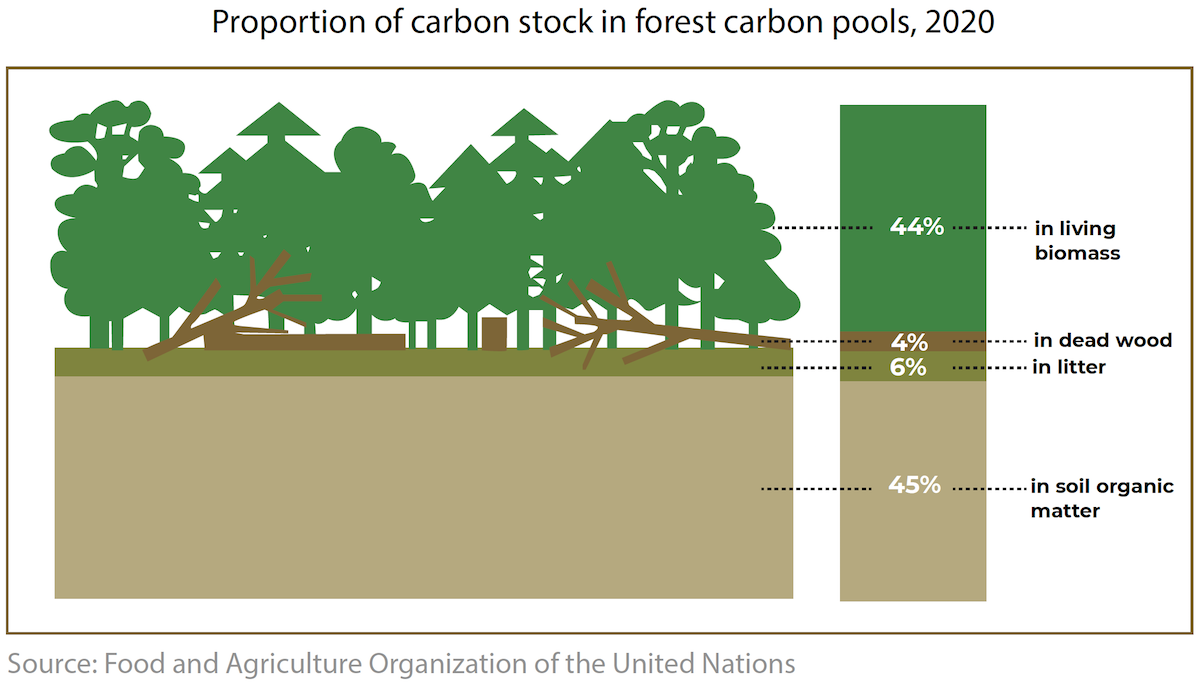

Deforestation is a significant threat to the carbon budget timeframe. Not only does it reduce the capacity to turn CO2 into carbon-storing biomass, but the means by which this happens, specifically fire, creates a net increase in the CO2 that is released. The United Nations ‘Food and Agriculture Organization’, in its 2020 key findings, estimated that the world’s forests currently hold around 662Gts of carbon.

Reforestation is a key goal agreed at the recent COP, in Glasgow, but the trend is still towards deforestation for agricultural use, mainly in South America and Africa. There is also the concern that weather extremes, caused by current levels of global warming, will increase the number and severity of forest fires.

Phytoplankton turn the oceans of the world into another main carbon sink. These microscopic algae currently absorb as much carbon as all the plants and trees on land combined. The combination of plankton-eating dumped microplastics, and acidification-driven changes in the oceanic ecosystem mean that the constancy of this source of CO2 removal is under considerable doubt.

Carbon Capture and Sequestration (CCS) is also a big unknown. Much of the climate change mitigation research, currently being conducted, is in this area, and most pathways that lead to either 1.5- or 2-degree limits, involve significant periods in the latter half of the century of net negative emissions, where more CO2 is removed than emitted.

These factors taken together result in a situation where the carbon budget as a destination has many possible routes.

Economics, tipping points, and feedback loops will determine policy…

The global carbon budget is known by governments who make up the UN, and who attend the COPs, but individual limits and policies are determined locally within each country. The shared aim to limit global warming is, therefore, tempered by their specific economic needs. This means that even though the required actions are reasonably well-understood, the timing of policy and implementation is less than certain.

The agreement at COP26 to annual reporting against, and increasing of, self-set targets will undoubtedly focus attention, but other factors may come into play.

The fact that global warming increases the likelihood of extreme weather events is now an accepted one, and there are other positive feedback loops within the ecosystem to consider – from unplanned forest fires, through oceanic biodiversity loss, to melting ice caps. All of these accelerate the impacts of global warming and are likely to force more urgent action from policymakers around the world.

Banks must work with current pathways…

The Intergovernmental Panel for Climate Change (IPCC) researches and publishes pathways that could result in the world achieving its global warming targets. These set out the actions that must be taken across a range of areas including:

- Industry

- Transportation

- Agriculture

- Land Management

- Infrastructure

- Construction

The question is less about what a pathway requires, but rather the speed at which it is put into place. Therefore, there are generally three sub-scenarios applied to each pathway, for comparative purposes. These are:

- Orderly – This is defined as a program that is planned and put into place early, to achieve a transition to a sustainable economy that businesses and populations can work with, without sudden, stringent measures. The costs here are significant and must be budgeted in a way that allows the economy to prepare for and absorb them without crisis.

- Disorderly – This is defined as taking little or no action until absolutely required, leading to significant business disruption. Regulatory changes, without notice, damage supply chains and limit firms’ capacity to adapt appropriately. This economic damage may hurt the ability to fund the required changes and cause liquidity issues throughout the system.

- Hothouse World – This is defined as doing nothing but adapting to the physical effects that global warming creates. This is not viewed as a viable alternative but is used to illustrate the endpoint of simply continuing on the same economic path as currently followed.

Each of these has a different impact on the businesses that make up the economy of each country. All these will have a mixture of positive and negative effects on firms’ business models and therefore, their credit profiles as customers of the bank.

An orderly transition is likely to impose adaptation costs on businesses, reducing their liquidity, but these will be signaled ahead of time and are likely to be introduced over a period of time. These are certainly costly, but likely manageable by most firms across various sectors.

A disorderly transition means that firms who look to apply non-regulatory changes may not be able to compete, and when regulations are changed, the timescales for compliance are most likely too short for proper investment. Essentially, an adaptation-led liquidity crisis should be expected.

As banks build climate-based scenarios for risk management purposes, both of these must be considered.

Banks can incentivize sustainability…

The fact that banks can run scenarios and see the future impact on their balance sheets implies that they can also take steps to avoid liquidity issues.

The results of climate scenarios will allow risk departments to see the credit-adjusted impact of this transition. Although this impact will come later, it does not change the overall cost to banks in terms of funding an increasing ‘Risk Weighted Asset’ capital charge against facilities granted before various climate regulations come into effect.

Impacts in terms of dollar costs can be applied by using the official ‘Net Greening of the Financial System’ (NGFS) estimates against each pathway option.

Banks can then:

- Estimate the change in regulatory capitalization caused to the loan book by each scenario assuming borrowers only take action when forced to.

- Estimate the difference in the costs if firms took early, pre-emptive action in sustainability – taken using IPCC action recommendations.

- Work the difference, by sector, into a green loan pricing policy.

- Set sustainable business targets using these capital indicators.

- Make monitoring of these targets a part of day-to-day bank governance.

The important fact here is that the required actions and implications of (not) taking them are already known. There is no need to wait for government regulation to measure these impacts, or to take steps to avoid them. Banks can become the catalyst of change, rather than simply its financial conduit.

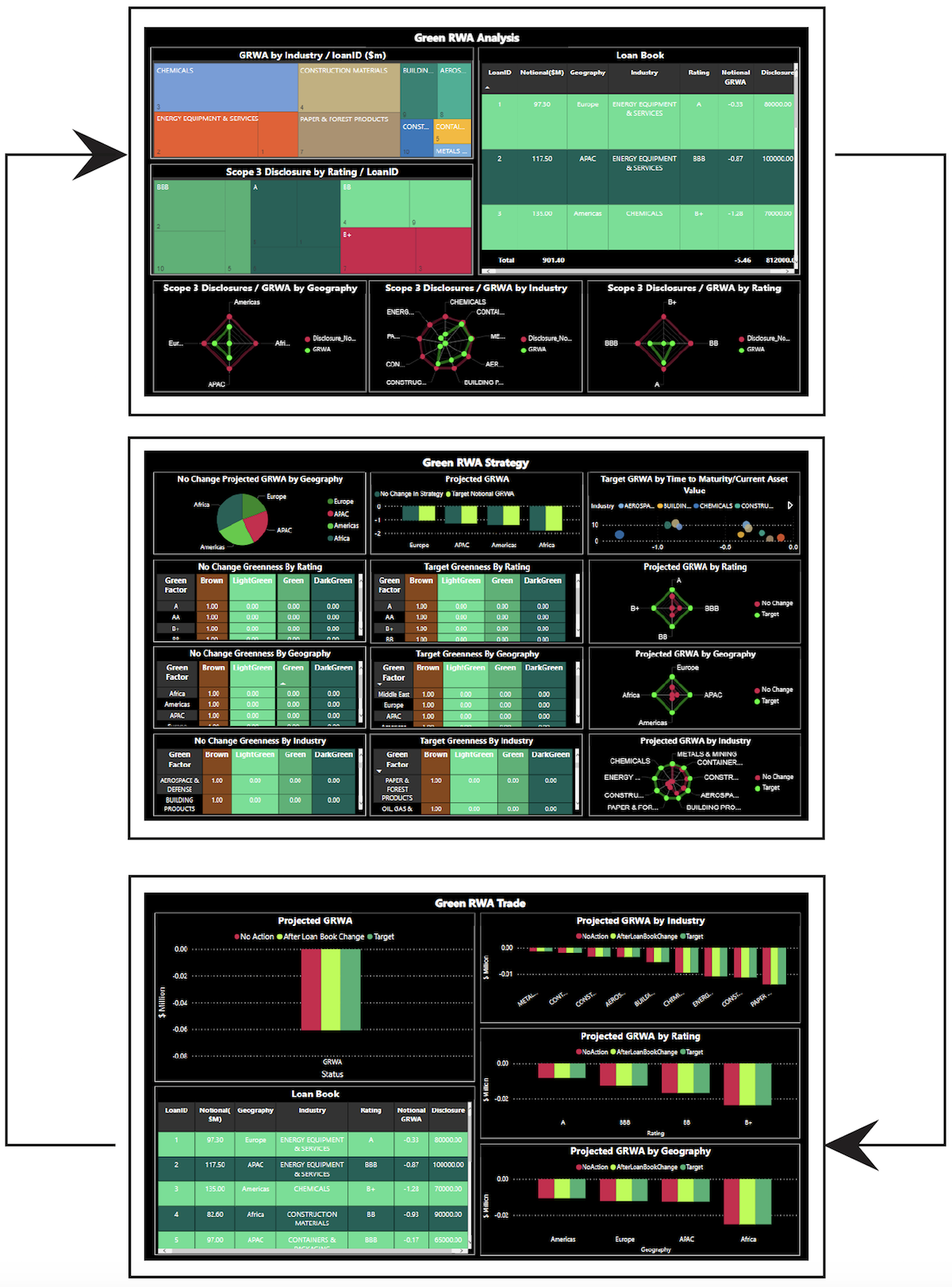

GreenCap can help…

GreenCap is a stand-alone ‘Risk As A Service’ (RAAS) solution that provides banks with the tools they need to apply scenarios to their balance sheets over the next 10 critical years. The system supplies reports on the current ‘no action’ increase in regulatory capital, as well as the means to apply bank-wide targets and loan-level adaptation savings.

Using GreenCap, banks can work with their customers to finance the changes that must happen over the coming decade, as well as pre-empt any liquidity issues by smartly calibrating known scenarios against a decreasing global carbon budget.