Carbon pricing schemes are core weapons in the fight against climate change, and their impact will have significant consequences for banks’ balance sheets

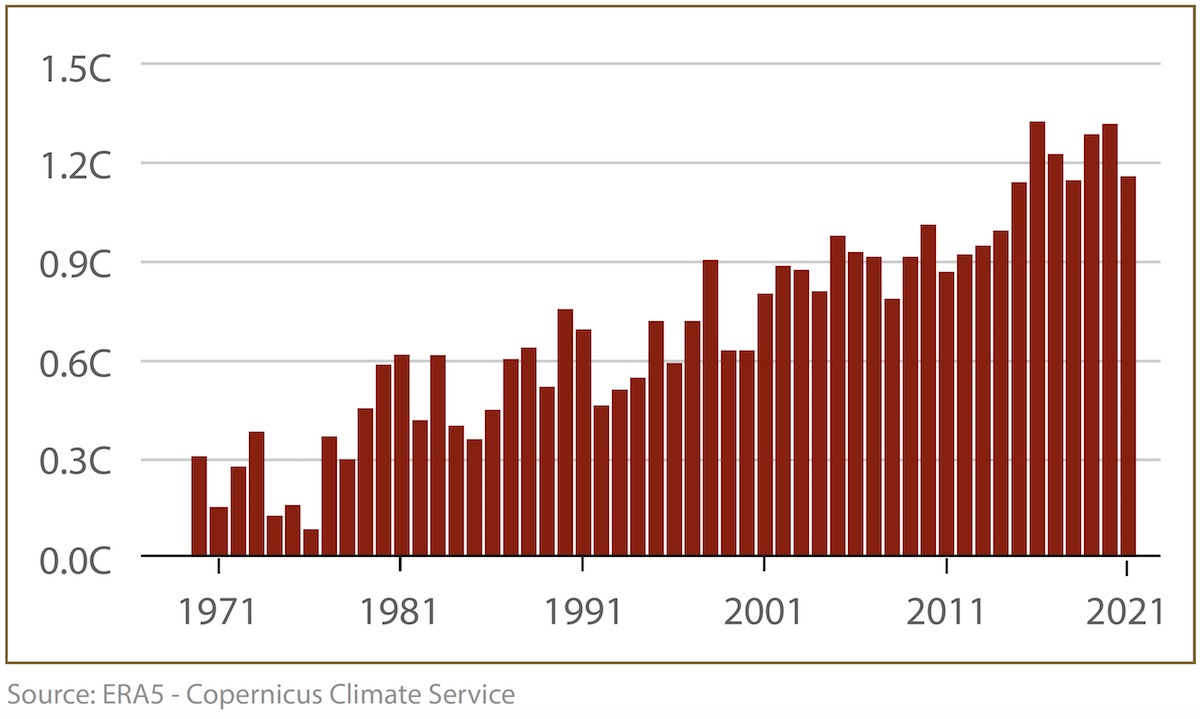

The year 2021 was officially the 5th warmest year on record and adds to the tally that see the last seven years as the seven warmest since the industrial revolution. 2021’s temperature is a particularly stark result given the ‘La Nina’ effect that would typically dampen the global warming impact.

This is accompanied by the consistently increasing accumulation of CO2 in the atmosphere, which continues to rise, despite commitments from world leaders to reduce emissions of the gas since the Conference of Parties (COPs), in Kyoto (1998) and Paris (2016).

Carbon pricing schemes are becoming a necessity…

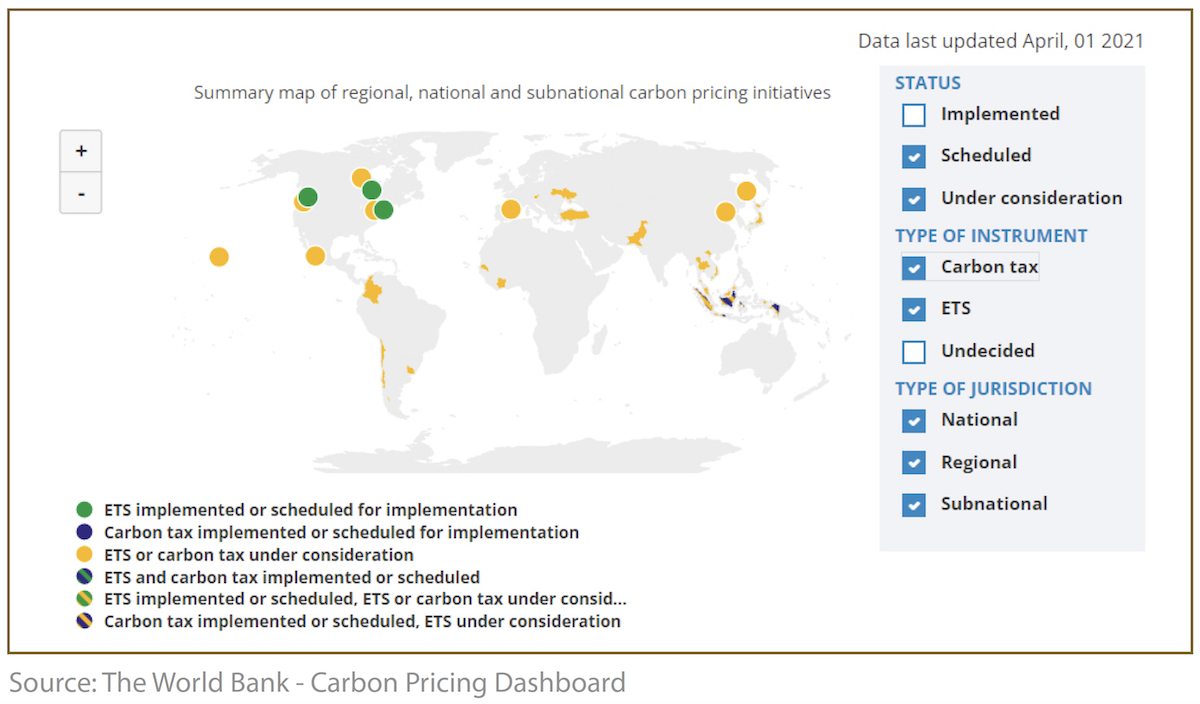

The urgency of curtailing CO2 emissions has led to the creation of carbon pricing schemes around the globe. There are two distinct types of carbon control – direct taxation of CO2 and carbon trading schemes and each has specificcharacteristics.

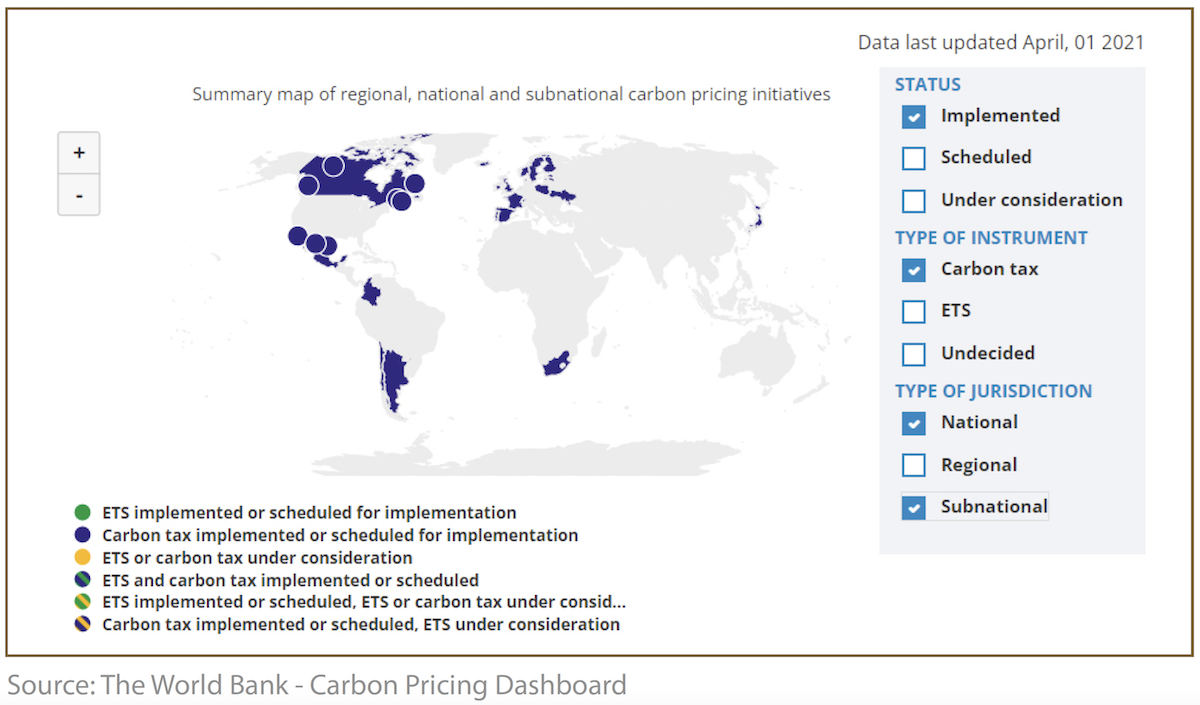

Carbon taxes represent the most direct means of charging for emissions. Currently, 27 national and 8 regional governments have charges in place, which force emitters to pay a set amount per tonne of gas produced.

The exact pricing of a tonne of gas varies by jurisdiction, but all are expected to rise as the national CO2 reduction targets become more aggressive through the 2020s. This emission controlling method allows comprehensive pricing to be applied and is transparent, making it useful for business planning purposes. Crucially, though, a carbon tax does not explicitly limit the amount of CO2 being released into the atmosphere.

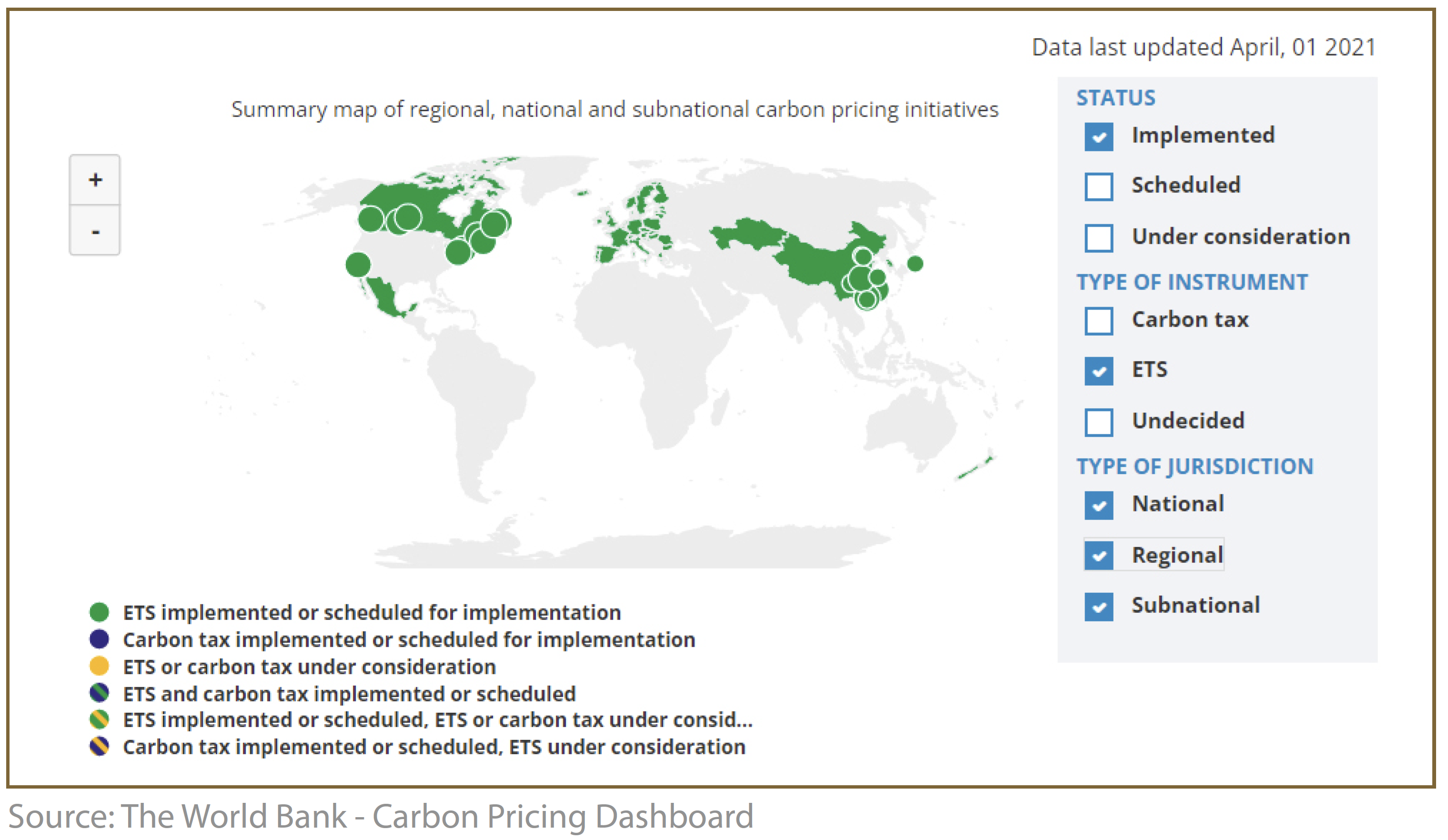

The alternative to a carbon tax, an Emissions Trading Scheme (ETS), is also popular in several countries and regions. This includes the EU, which has instituted a bloc-wide ETS.

It should be noted that while there is no federal ETS or carbon tax in the US, several states have independently implemented a trading system locally. ETSs are sometimes called ‘Cap and Trade’ systems and have the following basic features:

- A total cap is set on the emissions from the covered area, and by the covered industries/sectors

- This total is converted into notional carbon credits

- A percentage of the credits are allocated for free to specific emitters

- The remainder are normally auctioned off to the highest bidders

- Unused credits can then be traded in a valid carbon market

- The total emission allowance, and therefore the number of available credits, is reduced annually

ETS schemes have an advantage by being highly targeted by industry, and create an absolute, decreasing limit, in a way that general carbon taxes do not. That said, it is possible to build up a surplus of unused credits in the market, and there is no minimum price. These two issues result in an economic downturn, potentially making greenhouse gas emission rights cheap to buy on the open market, and thereby working against their designintent.

The EU has a highly developed ETS…

The EU implemented its ETS in 2005, and it currently stands as the largest in the world. Under the scheme, Greenhouse Gasses (GHGs) that are emitted by power plants, industrial factories, and the aviation sector are limited by a decreasing total ‘cap’.

The EU ETS provides equivalency between CO2 and Nitrous Oxide (N2O) or Perfluorocarbons (PFCs), making it a comprehensive GHG control, rather than just a limit on carbon emission. Between 2021 and 2030, the emission cap is set to decrease by 2.2% per annum. This is an increase from 1.74% that prevailed from 2013 to 2020.

The allowance of international credits, coupled with the economic crisis of 2008, led to a surplus of credits in the market. The EU dealt with this via a postponement of the auction of 900 million credits and the establishment of a Market Stability Reserve (MSR). The reserve is used as a price control by holding back excess credits, and a potential source of liquidity for credits if needed.

The increased reduction rate and use of the MSR are designed to maintain a GHG price level that disincentivizes processes that would prevent the bloc from achieving its ‘Green Deal’ objectives. Equally important is the expansion of the ETS to include maritime shipping and closer checks on ‘leakage’.

The two scheme types work in tandem, to create a market price…

With the two types of carbon pricing in active use, a global price for CO2 emission emerges. As border taxes, regime arbitrage, and cross-market credits develop, this price will stabilize and be usable as a guide to plan future additional business costs across economies and sectors.

Banks should take note of the growth of carbon pricing plans…

The EU is ahead but far from alone in the maturity of its carbon pricing. Along with the 45 countries with active schemes, which currently account for 22.5% of GHG emissions globally, plans are being discussed for several more around the world.

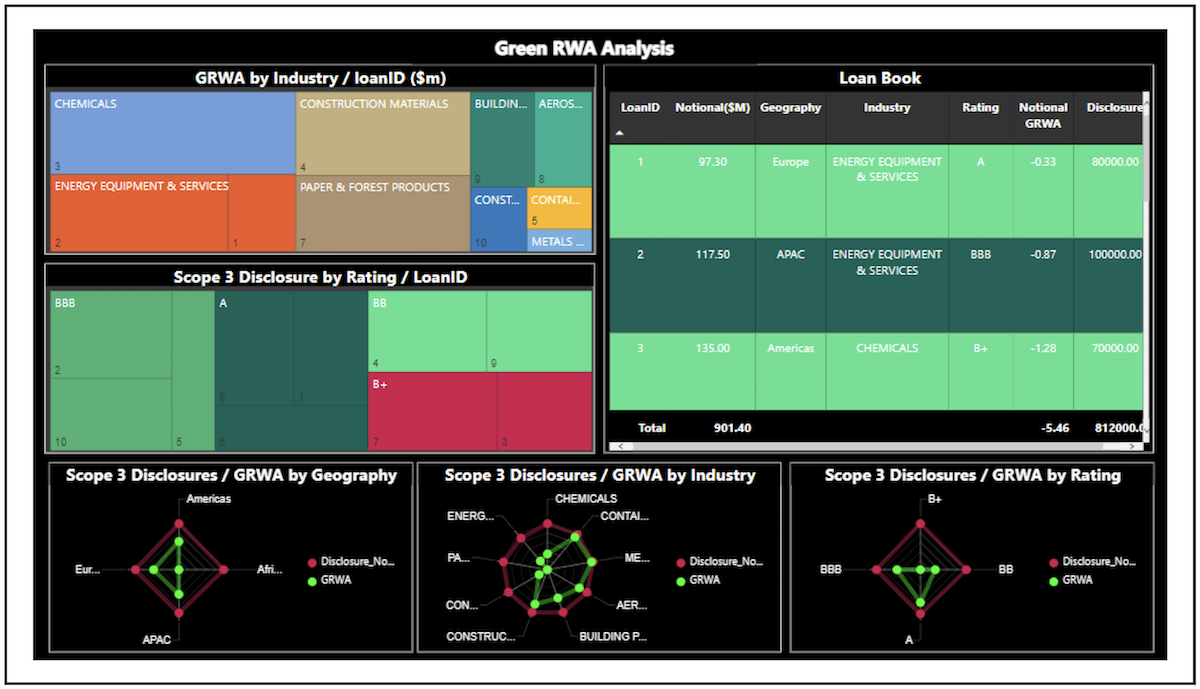

Banks are currently engaged in monitoring and reporting their ‘Scope 3’ emissions, which equate to the CO2 they finance through loans and other credit facilities. Taken with careful analysis of the carbon pricing schemes in production or development, they can:

- Use climate pathways developed by the International Panel on Climate Change (IPCC)

- Set costs against those pathways as developed by the Net Greening of the Financial System (NGFS)

- Attribute costs to obligors according to industry and estimated impact

- Use the currentemissions’ costs generated by the carbon pricing market

- Fine-tune the attributable cost to business, making up the balance sheets according to their adaptation actions and CO2 reduction plans

- Re-price loans and facilities to reflect the changing cost environment

- Become green finance centers, based on scientifically-based sustainable incentives to borrowers

All data needed to begin this work and set up the internal businesses and processes is available, and the accuracy of that data will increase through the coming decade as national and regional targets firm up towards 2030.

GreenCap can help…

GreenCap is a stand-alone ‘Risk As A Service’ (RAAS) system that enables banks to consolidate their balance sheets in terms of Scope 3 emissions and the additional risk capital that will be expected to be reserved from the additional credit risks arising from the underlying borrowers’ exposure to the increased risks from climate change policy and carbon pricing.