It is imperative for banks to work with developers to ensure a sustainable built environment

- As the COP26 conference in Glasgow approaches, governments around the world are seeking solutions to enable them to meet their self-set targets to create a CO2-neutral world by 2050.

- Spending commitments in Europe & the US are already colossal, but are also less than a third of the estimated requirement. This means that the private sector will have to find the rest, while being corralled and coerced through subsidy and regulation.

- Banks are critical for this work.

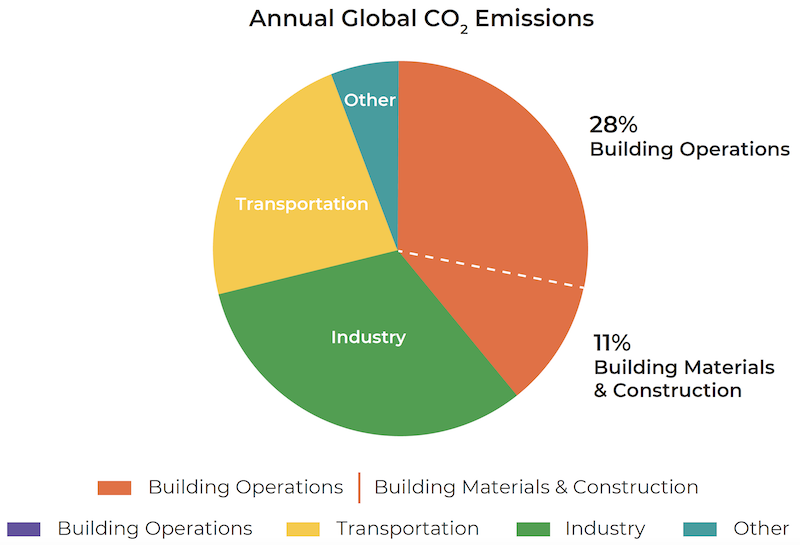

Buildings are prime targets for sustainable regulation. Accounting for 39% of total CO2 emissions, building construction (11%) and operation (28%), are areas where immediate and drastic action is needed to hold global warming to under 2 degrees, by 2100. Greenhouse gas emission reduction in these areas will involve changes to regulations for new buildings as well as massive investment in the adaptation of existing building stock—⅔ of which is expected to still be in use by 2050.

Banks will face significant changes to the borrowers’ credit profiles in this sector as project costs to meet new regulations increase, and the values of existing buildings (the collateral on many such loans) plummet to incorporate the price of adaptation.

Tracking a sustainable future…

The International Energy Agency (IEA) tracks the progress of various sectors with regard to sustainability goals. The building sector is graded as follows:

Building Envelope – This is defined as the exterior shell of the building that creates a barrier between the conditioned and unconditioned environment. The key to determining the ultimate energy needs includes both weather and heat protection. Therefore, it is a core concern for policymakers. The IEA grades this area as ‘not on track’.

Heating – This covers how the building is actively heated, from wood-burning fireplaces to solar-powered electrical heaters. The IEA grades this area as ‘not on track’.

Heat Pumps – Heat pumps are specifically targeted, as the adoption of geothermal heating for water and air is seen as key to sustainability in the future. Hence, heat pumps are increasingly adopted in new builds, but are still a costly adaptation to an existing building. The IEA grades this area as ‘more effort needed’.

Cooling – Cooling building interiors is more important than heating them in several parts of the world, and the current locked-in global warming is increasing these extremes. This sector is crucial to progressive designs and adaptation if buildings are to remain usable as we move through the century. The IEA grades the area as ‘more effort needed’.

Lighting – Lighting systems used in buildings have had the most impressive innovation, energy efficiency, adoption, and impact. The IEA grades this area as ‘on track’.

Appliances and Equipment – This area is where replacement and adaptation are likely to be a far bigger issue than innovation and adoption in new builds. The IEA grades this area as ‘more work needed’.

Overall, The IEA has the buildings sector set at ‘not on track’. This clearly implies that policymakers around the world have to act urgently in terms of regulations on new and existing stock, to even remotely meet the net neutral, mid-century targets. Banks should consider this a major short- and mid-term risk to collateral value and their balance sheets’ credit profiles.

Governments are already taking action…

The EU recently announced policies to make the ‘Green New Deal’ ambition a reality. The overall plan is to cut CO2 emissions by 55% by the year 2030. For the building sector its aims include:

- Part of the 72.2 billion euro spend (over 7 years) is earmarked for building renovation.

- A target of 49% of energy used in buildings to come from renewables by 2030.

- Member states must renovate at least 3% of public building floorspace annually.

- Member states must increase renewable energy in heating and cooling by at least 1.1% per year until 2030.

Some standards exist…

Countries around the world, including the US, have already started using the International Green Construction Code (IGCC), which details sustainability standards and certifications that are applied to high- and low-rise buildings. These standards cover a wide range of topics including:

- Sustainable sites

- Energy efficiency

- Water efficiency

- Materials and resource use

- Indoor environmental quality

- Greenhouse gas emissions

- Operations and maintenance

These standards apply equally to new builds, additions, and renovations. Effectively, buildings can be assessed from a bottom-up perspective using this code in the same way that the overall built environment can be assessed from a top-down perspective using the IEA reporting. These twin perspectives would enable banks to form a view of the size and cost of the overall risk, as well as to be able to accurately judge their own exposure to that risk.

Banks must be active during the transition…

The banking system will be at the center of this green transition. The need for private finance, coupled with the need for builders and owners to comply with new and upcoming regulations implied that property values may be quite volatile. This pressure imposed on those building firms and owners will translate into balance sheet credit changes and capital provisions for banks. At the very least, banks must:

- Be familiar with the changing regulatory landscape in the building sector.

- Understand the impact on their current balance sheet.

- Be prepared to work with and encourage customers to adopt sustainable building practices.

- Price credit facilities and loans accurately to reflect the risk from climate change and policies designed to combat it.

- Create short-, mid-, and long-term strategies to manage the climate change risk along with their customers.

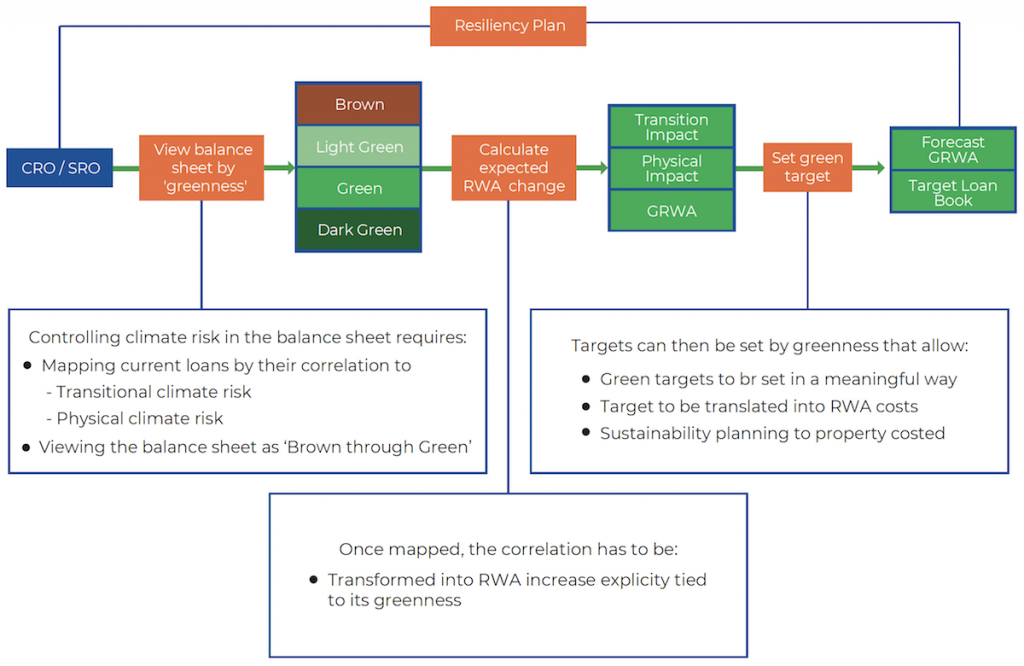

Greencap is designed to translate the real-world risks of physical and transitional climate change into a meaningful financial impact on banks and their balance sheet/profitability. It is intended to be a base for setting sustainability strategies and working directly with customers to achieve an economically viable, greener future.